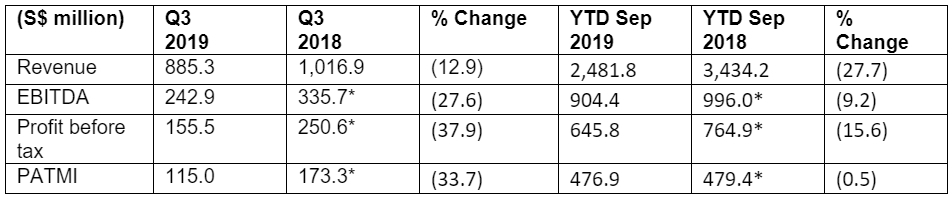

Singapore, 12 November 2019 – For the current quarter (Q3 2019) and nine months ended 30 September 2019 (YTD Sep 2019), City Developments Limited (CDL) achieved revenue of S$885.3 million (Q3 2018: S$1.0 billion) and S$2.5 billion (YTD Sep 2018: S$3.4 billion) respectively. The lower revenue contribution was due to the timing of revenue recognition for the property development segment.

Net attributable profit after tax and minority interest (PATMI) for Q3 2019 was S$115.0 million (Restated Q3 2018: S$173.3 million) and S$476.9 million for YTD Sep 2019 (Restated YTD Sep 2018: S$479.4 million), impacted significantly by impairment loss of approximately S$37 million made on two M&C hotels, Millennium Hilton Seoul and Millennium Hilton New York One UN Plaza, and the accrual of transaction costs following M&C’s successful delisting in October 2019.

{kind=image}

*Restated

# Important Note on Q3 and YTD Sep 2019 Revenue, PATMI and Basic Earnings Per Share

- The decrease in revenue was largely attributable to the timing of revenue recognition for the property development segment. The contributions from this segment tend to be lumpy as profits from some projects cannot be recognised progressively but only upon completion. In addition, the decline in PATMI was impacted by impairment losses on the two M&C hotels and costs for M&C privatisation. Excluding the impairment and privatisation costs, PATMI would have declined by 11.4% for Q3 2019 but would have increased by 8.9% for YTD Sep 2019.

- Basic earnings per share (EPS) stood at 12.7 cents for Q3 2019 (Restated Q3 2018: 19.1 cents) for Q3 2019 and 51.9 cents for YTD Sep 2019 (Restated YTD Sep 2018: 52.0 cents). Excluding impairment losses for hotels and costs of M&C’s privatisation, basic EPS would have declined by 11.5% to 16.9 cents for Q3 2019 but would have increased by 9.4% to 56.9 cents for YTD Sep 2019.

Operations Review and Prospects

Healthy Residential Sales in Singapore, China and other Overseas Markets

- In Singapore for YTD Sep 2019, the Group and its joint venture (JV) associates sold 1,130 units including ECs with total sales amounting to S$2.56 billion, reflecting an almost 44% increase in units sold with about 64% increase in sales value achieved, compared with the corresponding period last year (YTD Sep 2018: 787 units with sales value of S$1.56 billion).

- The Group launched six residential projects in 2019 – five projects for YTD Sep and one in Q4.

- March: Boulevard 88, the 154-unit ultra-luxurious JV development located along Orchard Boulevard has sold 83 units to date, achieving an average selling price (ASP) of over S$3,800 per square foot (psf). This freehold project, which is part of the Group’s legacy landbank, is not subject to time pressures. The Group has not been actively marketing the project, and with no time constraints, it will manage the release of the remaining units depending on market conditions.

- May: The 592-unit freehold JV project Amber Park located at East Coast has sold 188 units of the 200 released to date, at an ASP of around S$2,480 psf.

- July: The 188-unit Haus on Handy, located across the road from Dhoby Ghaut MRT station (a triple-line interchange station), has to date sold 30 units of the 40 released at an ASP of around S$2,870 psf.

- July: The 820-unit Piermont Grand EC at Punggol is the first and only EC project launch in 2019. To date, 444 units have been sold at an ASP of S$1,080 psf. It is located near two LRT stations linking to Punggol MRT station and close to the upcoming Punggol Digital District, which is poised to be Singapore’s Silicon Valley. The Group expects sales to remain strong with the recent policy changes raising EC income from S$14,000 to S$16,000.

- July: The 156-unit Nouvel 18, under the Group’s Profit Participation Securities (PPS) 3 initiative, is being marketed by the Group. To date, 24 units out of the 30 released have been sold at an ASP of above S$3,450 psf. Majority of the units in Nouvel 18 are leased out.

- November: The Group launched the 680-unit Sengkang Grand Residences in the heart of Sengkang Central – a JV with CapitaLand Limited. The residential towers of this distinctive integrated development are seamlessly connected to a three-storey mall (Sengkang Grand Mall), other lifestyle conveniences such as a community club, hawker centre, community plaza and childcare centre, as well as Buangkok MRT station and a new bus interchange. 216 of the 280 units released were snapped up on its launch weekend, making Sengkang Grand Residences the best-selling integrated project launch this year. To date, 232 units have been sold at an ASP of around S$1,700 psf.

- In China for YTD Sep 2019, the Group’s wholly-owned subsidiary CDL China Limited and its JV associates sold 420 residential units, achieving sales value of RMB 1.39 billion (approximately S$269 million).

- In the UK, the Group has seen some positive uptake for its London projects:

- Hans Road, Knightsbridge (three units): fully sold at an ASP of £4,176 psf.

- Sydney Street, Chelsea (nine units): two units have been reserved.

- Chesham Street, Belgravia (six units): one unit has been sold at an ASP of over £4,000 psf while another three units have been leased out.

- Teddington Riverside, Borough of Richmond upon Thames (Phase 1 – 76 units): 10 units have been sold at an ASP of about £1,388 psf, and another 19 units have been leased out.

- In Australia, the Group has sold over 50% of its JV 195-unit freehold residential project (The Marker) in West Melbourne.

Upcoming Launch in Singapore

- The Group’s residential GLS site at Sims Drive is being developed by its JV partner, Hong Leong Holdings Limited, and slated for sales launch in Q1 2020. Located near Aljunied MRT station and within an established residential estate, this residential project will comprise about 560 units.

Driving Recurring Income Growth with Asset Enhancement Initiatives (AEIs) and Strategic Acquisitions

AEIs

- In Singapore, following an extensive S$70 million AEI of the Group’s flagship commercial property Republic Plaza at Raffles Place, post-AEI rents achieved more than 10% higher than pre-AEI rents. This enhanced asset is expected to continue achieving positive rental reversions and increased income contribution.

- In the UK, M&C completed the £60 million refurbishment of its Mayfair property in London into a five-star deluxe hotel with 256 guest rooms and 51 designer suites. Rebranded as The Biltmore Mayfair, the hotel has just reopened on 9 September and is managed by Hilton under its luxury LXR Hotels & Resorts brand. As this is a management-franchise model, the Group has the option, after five years, to assume management of the hotel while maintaining the quality of the brand and leveraging Hilton’s reservations and loyalty programme.

Strategic Acquisitions

- In Japan, the Group entered into a sales and purchase agreement with Basis Corporation to acquire three freehold residential projects in Osaka City with a total of 130 apartments for JPY 3.45 billion (approximately S$44.3 million). One of the projects was completed in September 2019 and the other two are under construction and are due to complete by Q1 2020. Along with the acquisition of the freehold 34-unit Horie Lux residential development in Osaka announced in Q2 2019, the Group’s total "Build-to-Rent" assets in Japan now amount to JPY 5.46 billion (approximately S$69.3 million), with 164 units in total.

Successful Privatisation of M&C

- M&C was delisted from the London Stock Exchange on 11 October 2019 following the Group’s successful privatisation bid that was first announced on 7 June 2019. On 4 November 2019, M&C was re-registered as a private company under the name of Millennium & Copthorne Hotels Limited.

- On 19 November 2019, the Group expects to compulsorily acquire all the issued shares held by M&C shareholders who have not accepted the Final Offer. M&C will then become a wholly-owned subsidiary of the Group.

Mr Kwek Leng Beng, Executive Chairman of CDL, said, “The successful privatisation of M&C marks a key milestone in the Group’s transformational journey. Taking M&C private is in line with the Group’s core focus to enhance recurring income. With full control of M&C, the Group will take a holistic review of its hotel operations segment. We will embark on an internal restructuring to improve organisational processes and drive operational efficiency to create sustainable hotel performance amid global economic headwinds and stiff competition faced by the hospitality industry.

Alongside these challenges lie opportunities to create value and we will navigate this with agility. We plan to accelerate M&C’s integration with initiatives that will maximise shareholder value. These include controlling and reducing operating costs acutely; leveraging the Group’s global network, resources and real estate capabilities to refurbish assets for enhanced growth – especially those with conference facilities; repositioning underperforming assets and exploring the development of unutilised land.”

Mr Sherman Kwek, Group Chief Executive Officer of CDL, said, “Although the Singapore property market continues to face challenges arising from a supply overhang, CDL’s residential launches in Singapore have achieved relatively healthy sales. This reflects the underlying demand for homes with compelling value propositions that are anchored down by strong locations, high quality standards and outstanding design. In the meantime, we continue to accelerate our global expansion, purchasing both development sites and investment properties in our core overseas markets of UK, China, Japan and Australia. These highly selective acquisitions will support the crystallisation of our fund management ambitions and help to grow our recurring income. Another focus has been on enhancing our existing portfolio such as the recent revamp of our flagship office building Republic Plaza, which yielded positive rental reversions. We are actively pursuing other redevelopment opportunities or AEIs to extract greater value from our assets. Together, all the initiatives above demonstrate our relentless execution of the GET strategy of Growth, Enhancement and Transformation.”